Doprava zdarma se Zásilkovnou nad 1 499 Kč

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 74 Kč

Zásilkovna 49 Kč

PPL 99 Kč

Jak nakupovat

Jak nakupovat

Pomoc

Doručení

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 74 Kč

Zásilkovna 49 Kč

PPL 99 Kč

Doprava zdarma se Zásilkovnou nad 1 499 Kč

Nákupní rádce

Jsme tu pro vás!

571 999 090

Můj účet

Staňte se součástí komunity milovníků knih z celého světa a získejte hromadu výhod.

Založit účet zdarma

▸

Prázdný :-(

0

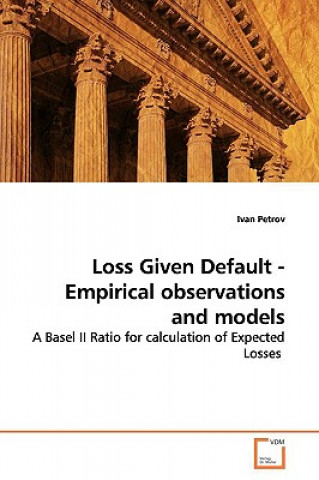

Loss Given Default - Empirical observations and models

Jazyk

Angličtina

Angličtina

Angličtina

Kniha

Brožovaná

In times of implementation of Basel II Approach and§financial crisis, the importance of Loss Given§D...

Celý popis

Libristo kód: 06826067

?

138 b

138 b

138 b

1 375

Kč

včetně DPH

Skladem u dodavatele

Odesíláme za 15-20 dnů

30 dní na vrácení zboží

Mohlo by vás také zajímat

In times of implementation of Basel II Approach and§financial crisis, the importance of Loss Given§Default (LGD), as a measure of expected losses by default§of banks, companies, corporations, etc. will increase§rapidly. The understanding of central statistical§characteristics of LGD will help the Banks, Hedge§Funds and other Lending Parties to forecast and§measure the potential losses, if a company goes§bankrupt. For its prediction should be created new§accurate mathematical and risk management models and§therefore the involving parties should have more§empirical observations from the past and study the§existing models in that area.

Informace o knize

Plný název

Loss Given Default - Empirical observations and models

Autor

Ivan Petrov

Jazyk

Angličtina

Angličtina

Vazba

Kniha - Brožovaná

Datum vydání

2009

Počet stran

80

EAN

9783639178081

ISBN

3639178084

Libristo kód

06826067

Nakladatelství

VDM Verlag

Váha

127

Rozměry

152 x 229 x 5