Doprava zdarma se Zásilkovnou nad 1 499 Kč

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 74 Kč

Zásilkovna 49 Kč

PPL 99 Kč

Jak nakupovat

Jak nakupovat

Pomoc

Doručení

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 74 Kč

Zásilkovna 49 Kč

PPL 99 Kč

Doprava zdarma se Zásilkovnou nad 1 499 Kč

Nákupní rádce

Jsme tu pro vás!

571 999 090

Můj účet

Staňte se součástí komunity milovníků knih z celého světa a získejte hromadu výhod.

Založit účet zdarma

▸

Prázdný :-(

0

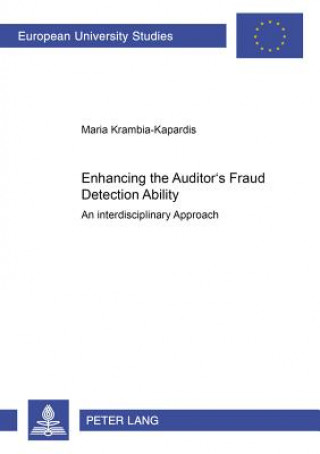

Enhancing the Auditor's Fraud Detection Ability

Jazyk

Angličtina

Angličtina

Angličtina

Kniha

Brožovaná

There has been much debate about the auditor's role in fraud detection. Since auditors lack sufficie...

Celý popis

Libristo kód: 10021619

?

158 b

158 b

Připravujeme

Připravujeme

158 b

Připravujeme

1 581

Kč

včetně DPH

Očekávaný dotisk

Termín neznámý

Termín neznámý

Termín neznámý

30 dní na vrácení zboží

Mohlo by vás také zajímat

There has been much debate about the auditor's role in fraud detection. Since auditors lack sufficient skill and experience to have a reasonable chance of detecting fraud, it is argued they should look to other disciplines for useful knowledge. This book draws on criminology, psychology and sociology to put forward a model of fraud aetiology which was tested in a study of major fraud offenders. Attention then focuses on a survey of auditor's experience in detecting material irregularities in the financial statements which tested the usefulness of an eclectic fraud detection model that includes the fraud aetiology model as one of its components.

Informace o knize

Plný název

Enhancing the Auditor's Fraud Detection Ability

Autor

Maria Krambia-Kapardis

Jazyk

Angličtina

Angličtina

Vazba

Kniha - Brožovaná

Datum vydání

2001

Počet stran

188

EAN

9783631369722

ISBN

9783631369722

Libristo kód

10021619

Nakladatelství

Peter Lang AG

Váha

266

Rozměry

210 x 149 x 12