Doprava zdarma se Zásilkovnou nad 1 499 Kč

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 74 Kč

Zásilkovna 49 Kč

PPL 99 Kč

Jak nakupovat

Jak nakupovat

Pomoc

Doručení

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 74 Kč

Zásilkovna 49 Kč

PPL 99 Kč

Doprava zdarma se Zásilkovnou nad 1 499 Kč

Nákupní rádce

Jsme tu pro vás!

571 999 090

Můj účet

Staňte se součástí komunity milovníků knih z celého světa a získejte hromadu výhod.

Založit účet zdarma

▸

Prázdný :-(

0

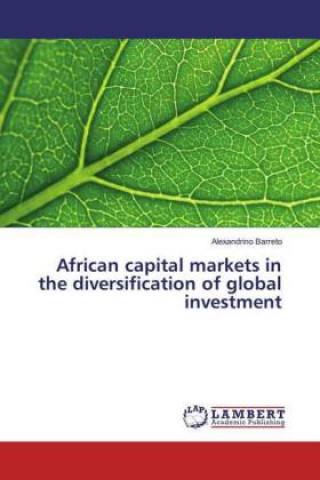

African capital markets in the diversification of global investment

Jazyk

Angličtina

Angličtina

Angličtina

Kniha

Brožovaná

This book addresses the issues of diversification at the international context. Furthermore, this bo...

Celý popis

Libristo kód: 19064419

?

86 b

86 b

86 b

861

Kč

včetně DPH

Skladem u dodavatele

Odesíláme za 9-11 dnů

30 dní na vrácení zboží

Mohlo by vás také zajímat

This book addresses the issues of diversification at the international context. Furthermore, this book adresses topics like In-sample and Out-Of-Sample approaches to analyze the data; optimization models to compose the efficient portfolios using models from classic to modern like Mean Variance (MV), Mean Absolute Deviation (MAD), Semivariance (SV), Resample Michaud (RM) and Filtered Historical Simulation (FHS); and bring the Matlab code for each optimization model that can be used in the future research. On the other hand, this book can help investors that seek to maximize return and minimize risk of the their portfolios using the African emergent markets.

Informace o knize

Plný název

African capital markets in the diversification of global investment

Autor

Alexandrino Barreto

Jazyk

Angličtina

Angličtina

Vazba

Kniha - Brožovaná

Datum vydání

2018

Počet stran

80

EAN

9786136830193

Libristo kód

19064419

Nakladatelství

LAP Lambert Academic Publishing

Váha

137

Rozměry

150 x 220 x 5